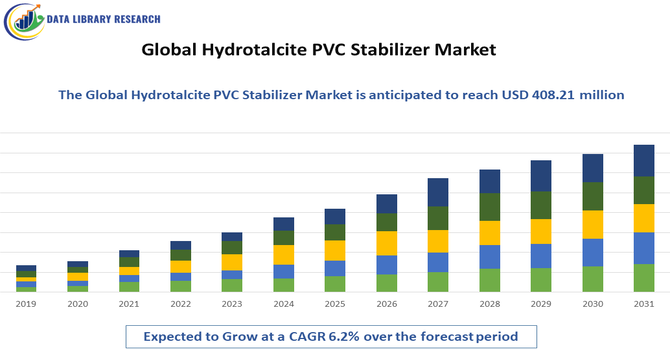

The Global Hydrotalcite PVC Stabiliser Market size was valued at USD 277.12 million in 2026 and is expected to reach USD 408.21 million by 2033, growing at a CAGR of 6.2% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Hydrotalcite PVC Stabiliser Market refers to the worldwide industry that produces and supplies hydrotalcite based additives used to enhance the thermal stability, processability, and environmental compliance of polyvinyl chloride (PVC) formulations. Hydrotalcite stabilisers are layered double hydroxides (typically magnesium and aluminum compounds) that replace traditional heavy metal stabilisers, especially where lead and cadmium are restricted by environmental regulations. Adoption is driven by increasing PVC consumption in construction, automotive, electrical and consumer goods applications, regulatory focus on non toxic additives, and innovation in hydrotalcite production and performance characteristics worldwide.

Key market trends include a shift toward eco friendly, non toxic stabilisers as stricter regulations phase out heavy metal additives and encourage lead free alternatives in PVC products. Technological advancements are improving hydrotalcite dispersion and thermal performance, enhancing product quality for high demand sectors like construction and automotive. The Asia Pacific region leads growth due to rapid industrialisation and rising PVC consumption, while digitalisation and Industry 4.0 practices optimise production efficiency. Growth in recycled PVC streams and hybrid stabiliser solutions also shapes product development, increasing demand for high performance, sustainable additives that align with circular economy goals.

Segmentation: The Global Hydrotalcite PVC Stabiliser Market is segmented by Product Type (Mg Al Hydrotalcite, Mg Al Zn Hydrotalcite and Other Hydrotalcite Variants), Physical Form (Powder Form and Granule Form), Application Type (PVC and CPVC Stabilizers, Polyolefin Processing, Flame Retardant Additives, Medical/Pharmaceutical Uses and Others), End Use Industry (Construction & Infrastructure, Automotive, Electrical & Electronics, Consumer Goods & Packaging and Other Industrial Sectors), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver for the hydrotalcite PVC stabiliser market is the global regulatory shift towards eco friendly, non toxic additives. Legislation in the EU, China, India and other regions restricts or bans heavy metal stabilisers such as lead and cadmium in PVC products, particularly for potable water applications, children’s goods, and food contact items. This has accelerated the adoption of hydrotalcite stabilisers that comply with stringent environmental and health standards. The trend towards sustainable materials and green building certifications further amplifies demand, as manufacturers seek safer alternatives without compromising performance in construction, automotive, and electrical applications.

Another significant driver is the rising global PVC consumption in key end use industries like construction, infrastructure and automotive manufacturing. PVC’s cost effectiveness, durability, and versatility make it a preferred material for piping systems, window profiles, wiring insulation and automotive components. As these sectors expand, especially in emerging economies across Asia Pacific and Latin America, demand for PVC stabilisers, including hydrotalcite grades, increases correspondingly. Growth in urbanisation, housing projects, electrification and lightweight automotive parts raises stabiliser requirements. Additionally, recycled PVC streams often require higher stabiliser loading, supporting further volume growth for hydrotalcite stabilisers.

Market Restraints:

A notable restraint for the hydrotalcite PVC stabiliser market is high production costs and raw material volatility. Synthesising high purity hydrotalcite requires energy intensive processes and tight control over chemical conditions, making manufacturing costs significantly higher than some conventional stabilisers. Dependence on magnesium and aluminum precursors exposes producers to fluctuating commodity prices and supply chain uncertainties, which can narrow profit margins and increase end product costs. Smaller polymer processors in price sensitive markets may resist switching to hydrotalcite additives due to cost constraints, limiting broader adoption despite performance and regulatory advantages.

The hydrotalcite PVC stabiliser market has significant socioeconomic impact by supporting safer polymer products that reduce human and environmental exposure to toxic heavy metals. Demand growth sustains jobs across mining, chemical processing, manufacturing, and downstream PVC value chains globally, particularly in emerging economies expanding infrastructure and automotive production. Regulatory compliance with environmental standards fosters healthier working and consumer environments. The rise of local production facilities in regions like Asia Pacific improves economic self sufficiency and trade balances. However, fluctuations in raw material costs impact pricing and accessibility of PVC products, influencing consumer prices in construction and consumer goods sectors.

Segmental Analysis:

The Mg Al hydrotalcite segment is expected to witness the highest growth over the forecast period because it currently holds the majority share and is widely adopted for PVC stabilisation due to its superior thermal stability, acid scavenging properties, and cost effectiveness compared with other variants. Its broad applicability in rigid and flexible PVC applications—especially where stringent environmental regulations are phasing out heavy metal stabilisers—supports this growth trajectory. Manufacturers favour Mg Al grades for construction, automotive and electrical applications due to their reliability and compliance with eco friendly standards. The transition toward halogen free additive systems further reinforces demand, making Mg Al hydrotalcite the leading growth segment.

The granule form segment of hydrotalcite PVC stabilisers is anticipated to see the highest growth among physical form categories during the forecast period. Granules offer superior handling, reduced dust generation, and improved dispersion during PVC compounding compared to powder forms, which enhances manufacturing efficiency and product consistency. These practical advantages support increased adoption in large scale industrial processes where ease of use and process optimisation are critical. Additionally, granule forms facilitate better automation compatibility in modern PVC compounding lines, aligning with Industry 4.0 trends. As manufacturers prioritise operational efficiency and worker safety, granule formats are expected to outpace other physical forms in market expansion.

Within application segments, the polyolefin processing segment is projected to experience the highest growth over the forecast period. While PVC stabilisation remains dominant, polyolefin markets—covering polyethylene (PE) and polypropylene (PP)—are expanding rapidly due to demand in packaging, automotive parts, consumer goods, and industrial components. Hydrotalcite serves as an effective acid scavenger and stabiliser in polyolefin formulations, improving thermal stability and processing characteristics such as melt flow during extrusion and injection moulding. Growth in global polyolefin consumption, especially in emerging economies with expanding manufacturing bases, supports higher uptake of hydrotalcite stabilisers in these applications compared with traditional additives.

The construction & infrastructure segment is forecast to witness the highest growth among end use industries for hydrotalcite PVC stabilisers. PVC materials are integral to modern construction—used extensively in piping systems, window profiles, roofing membranes, flooring and electrical conduits—owing to their durability, cost effectiveness, and ease of installation. Regulatory pressures in many regions have accelerated the shift from toxic heavy metal stabilisers to hydrotalcite based, eco friendly alternatives, especially in plumbing and potable water applications. Growing infrastructure investment, rapid urbanisation in emerging markets, and government housing initiatives further amplify PVC demand, directly driving increased consumption of hydrotalcite stabilisers in construction applications.

The Asia Pacific region is expected to demonstrate the highest growth for the global hydrotalcite PVC stabiliser market over the forecast period.

This region already accounts for a dominant share of global hydrotalcite consumption due to large scale PVC production and robust growth in end use sectors like construction, automotive, and electrical products. For instance, in November 2023, Baerlocher India’s launch of its GHG-optimized facility expanded sustainable PVC additive production, including calcium-based stabilizers and metal soaps, strengthening its position as a leading manufacturer and boosting the Asia-Pacific hydrotalcite PVC stabilizer market.

Rapid industrialisation, urbanisation, and substantial investments in infrastructure projects in countries such as China, India, Vietnam and Southeast Asian markets fuel escalating PVC demand. Additionally, tightening environmental regulations across Asia Pacific promote the adoption of non toxic hydrotalcite stabilisers over traditional heavy metal systems, further accelerating regional market expansion.

| Report Matrics | Details |

| Market Size Value | USD 408.21 million |

| Growth Rate | CAGR of 6.2% |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the hydrotalcite PVC stabiliser market is moderately consolidated, with multinational chemical companies and specialised regional players competing on product innovation, quality, and regulatory compliance. Leading firms hold a majority of global capacity, leveraging strong R&D, broad geographic reach, and diversified product portfolios to serve major PVC applications. Competition focuses on enhanced thermal stability, eco friendly formulations, and tailored solutions for construction, automotive and speciality PVC products. Regional production hubs and partnerships expand market presence, while digital optimisation and sustainability credentials increasingly differentiate competitors. Growth in Asia Pacific intensifies rivalry as local manufacturers scale capacity to meet rising demand.

The major players are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the global shift toward eco-friendly and non-toxic additives in PVC manufacturing. As regulations phase out lead-based stabilizers due to health concerns, hydrotalcite has emerged as a superior, sustainable alternative. Additionally, the booming construction and automotive sectors increase demand for high-performance, heat-stable PVC products.

Q2. What are the main restraining factors for this market?

The market is primarily restrained by the higher production costs of hydrotalcite compared to traditional lead or tin-based stabilizers. Volatility in raw material prices and the technical complexity of achieving the same stabilization efficiency in certain formulations also pose challenges. Furthermore, competition from other organic stabilizers can limit its adoption.

Q3. Which segment is expected to witness high growth?

The Mg Al hydrotalcite segment is projected to witness the highest growth over the forecast period due to its superior thermal stability, eco-friendly profile, and wide applicability in PVC products. Rising demand from construction, automotive, and electrical sectors, combined with regulatory shifts away from heavy-metal stabilizers, further accelerated adoption, making Mg Al hydrotalcite the fastest-growing segment in the global PVC stabilizer market.

Q4. Who are the top major players for this market?

Key industry leaders include Kyowa Chemical Industry, Clariant, Kisuma Chemicals, and AkzoNobel. Other prominent players such as Mitsui Chemicals, Doobon, and various specialized Chinese manufacturers like Hebei Jingu Group contribute significantly. these companies focus on R&D to improve the acid-scavenging efficiency and transparency of their hydrotalcite products.

Q5. Which country is the largest player?

China is the largest player in this market, both as a producer and a consumer. Its dominance is fueled by a massive PVC manufacturing base and increasingly stringent environmental regulations favoring non-toxic stabilizers. The country’s rapid urbanization and infrastructure development further solidify its position as the global hub for hydrotalcite.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model