Get Complete Analysis Of The Report - Download Updated Free Sample PDF

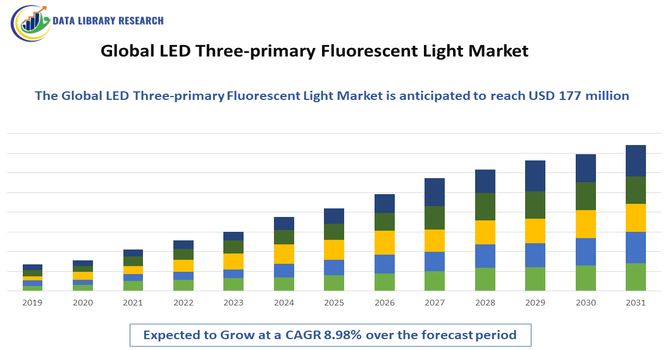

The Global LED Three primary Fluorescent Light Market encompasses lighting solutions that use LED technology with three primary fluorescent (or three primary color) characteristics, delivering enhanced color rendering, higher efficiency, and improved visual comfort compared to traditional lighting. These lights are widely used in commercial, industrial, and residential applications where accurate color reproduction and energy savings are important. Rapid urbanization, digital building systems integration, and sustainability mandates are driving adoption. Innovations in phosphor chemistry, smart controls, and IoT connectivity further boost utility and flexibility.

Market trends show a shift toward smart, connected lighting systems leveraging three primary fluorescent LED technology, integrating IoT and adaptive controls for optimized energy management. Advanced phosphor blends improve color accuracy and daylight mimicry, appealing to commercial and architectural applications. Sustainability regulations and energy codes push replacement of legacy fluorescent systems with higher performance LED solutions that reduce energy consumption and operational costs. Digital lighting networks with sensors and adaptive dimming deliver real time efficiency gains. Regional manufacturing expansions, particularly in Asia Pacific, increase production scale and lower costs, supporting wider global deployment across commercial, retail, and industrial sectors.

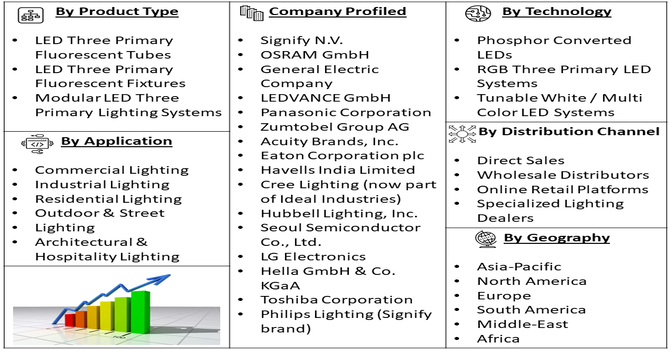

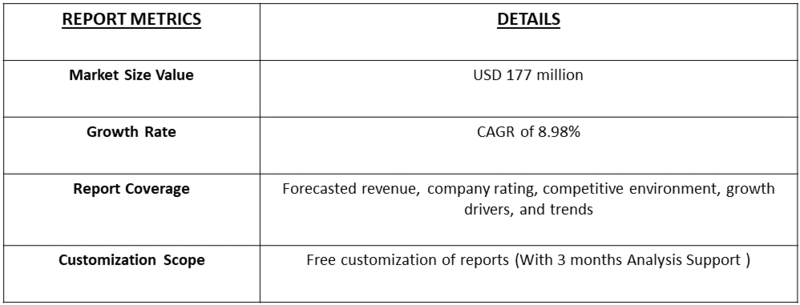

Segmentation: The Global LED Three primary Fluorescent Light Market is segmented by Product Type (LED Three Primary Fluorescent Tubes, LED Three Primary Fluorescent Fixtures and Modular LED Three Primary Lighting Systems), Technology (Phosphor Converted LEDs, RGB Three Primary LED Systems and Tunable White / Multi Color LED Systems), Application (Commercial Lighting, Industrial Lighting, Residential Lighting, Outdoor & Street Lighting and Architectural & Hospitality Lighting), Power Rating (Low Power (<20 W), Medium Power (20 – 100 W) and High Power (>100 W)), Distribution Channel (Direct Sales, Wholesale Distributors, Online Retail Platforms and Specialized Lighting Dealers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The key driver is stringent global energy efficiency and environmental regulations that push industries and governments to adopt sustainable lighting solutions. Policies phasing out inefficient fluorescent lamps and incentivizing high efficiency LED alternatives accelerate the shift toward three primary fluorescent LED lighting. These regulations aim to cut energy consumption, reduce greenhouse gas emissions, and meet climate targets, compelling commercial and public sectors to upgrade infrastructure. Enhanced color rendering and longer lifespans further appeal to specifiers seeking cost effective, durable products. As regulatory frameworks tighten worldwide, market demand grows for certified, high performance LED lighting systems that comply with energy codes and sustainability mandates, boosting overall market expansion.

Another major driver is the integration of three primary LED lighting with smart and IoT enabled control systems, appealing to modern building and urban infrastructure projects. Smart lighting networks use sensors, adaptive controls, and data analytics to optimize light levels and energy consumption dynamically. This capability enhances operational efficiency and reduces waste, making LED three primary solutions attractive for commercial, industrial, and public spaces seeking digital transformation. Integration with building management systems and energy dashboards enables predictive maintenance, real time monitoring, and lower lifecycle costs. As connectivity technologies evolve, the convergence of lighting and digital control systems fuels demand for advanced LED lighting products globally.

Market Restraints:

A significant restraint is intense competition from other advanced LED lighting technologies, such as tunable white LEDs, micro LEDs, and OLED systems that offer high efficiency and customizable spectra. These alternatives often deliver similar or superior energy performance, better design flexibility, or enhanced integration features. Additionally, the rapid pace of innovation in LED chips and lighting modules can outpace three primary fluorescent solutions, leading buyers to prioritize newer technologies. High initial costs for advanced three primary LED fixtures compared with standard LED tube lights can deter price sensitive segments, especially in emerging markets. Market fragmentation and shifting consumer preferences toward other LED formats could constrain growth.

The LED three primary fluorescent light market positively impacts economies by lowering energy demand and reducing operational costs for businesses and public infrastructure. Energy efficient lighting solutions support sustainability goals and compliance with regulatory standards, reducing carbon emissions and environmental burden. Broader adoption generates employment in manufacturing, installation, distribution, and system integration sectors. Enhanced lighting quality improves productivity in workplaces and public spaces, while reduced maintenance needs cut long term expenses. Urban infrastructure projects increasingly incorporate advanced LED solutions, stimulating construction and technology sectors. Additionally, improved visual comfort and safety in indoor environments contribute to better wellbeing and workplace performance globally.

Segmental Analysis:

The LED Three Primary Fluorescent Fixtures segment is expected to witness the highest growth over the forecast period due to increasing demand for integrated lighting solutions in commercial, industrial, and institutional applications. Fixtures offer better energy efficiency, uniform illumination, and ease of installation compared with individual tubes, making them suitable for offices, retail spaces, and warehouses. Rapid urbanization and infrastructure modernization projects drive adoption, supported by sustainability initiatives. Integration with smart lighting controls, IoT systems, and adaptive dimming enhances operational efficiency and user experience. Growing emphasis on energy savings and high-quality visual performance further fuels market expansion in this segment globally.

The Phosphor Converted LEDs (PC-LEDs) segment is projected to witness the highest growth due to their superior color rendering, energy efficiency, and long lifespan. PC-LEDs use phosphor coatings to convert blue or UV light into full-spectrum illumination, making them ideal for commercial, industrial, and residential applications where color accuracy and comfort are critical. Technological improvements in phosphor materials and LED chips reduce energy consumption while delivering consistent brightness. The cost-effectiveness and ease of integration with existing lighting systems further enhance adoption. Regulatory incentives promoting energy-efficient lighting solutions globally contribute to rapid growth of PC-LEDs within the three-primary fluorescent LED market.

The Medium Power (20–100 W) segment is expected to witness the highest growth, as it strikes a balance between performance and affordability for commercial, industrial, and institutional lighting needs. Medium-power LEDs provide adequate illumination for offices, retail spaces, warehouses, and educational facilities while maintaining energy efficiency and reduced operational costs. These LEDs are compatible with smart controls, sensors, and dimming systems, enhancing flexibility and utility. Rapid infrastructure development in emerging economies and retrofitting of conventional lighting systems worldwide further drives demand. This segment’s adaptability, optimal wattage, and favorable cost-benefit ratio make it a leading contributor to the global LED three-primary fluorescent light market.

The Online Retail Platforms segment is projected to witness the highest growth due to the increasing penetration of e-commerce in lighting products.

Consumers and businesses prefer online platforms for the convenience of comparing features, prices, and reviews before purchasing LED three-primary fluorescent lights. Platforms offer access to a wide variety of products, including fixtures, tubes, and smart lighting systems, catering to diverse end-users. Growth in B2B and B2C online sales, coupled with home delivery and easy returns, encourages adoption. Integration with digital marketing and direct manufacturer-to-consumer sales enhances accessibility. Rising internet penetration and the convenience of online shopping continue to expand this segment globally.

The Asia-Pacific region is expected to witness the highest growth over the forecast period, driven by rapid urbanization, industrialization, and infrastructural development in China, India, Japan, and Southeast Asia.

Rising awareness of energy-efficient lighting solutions, government incentives, and sustainability regulations encourage adoption of LED three-primary fluorescent lights. For instance, in 2022, CLASP partnered with the China National Institute for Standardization (CNIS) to assess LED adoption feasibility. The report highlighted a rapid decline in China’s fluorescent production and consumption, indicating that with government support, the shift to energy-efficient LED lighting could accelerate, significantly boosting growth in the Asia-Pacific LED Three Primary Fluorescent Light Market.

Strong manufacturing capabilities, low production costs, and local market expansion facilitate availability of cost-effective solutions. Commercial, industrial, and residential sectors are increasingly upgrading from conventional lighting systems, boosting demand. Technological advancements, coupled with integration into smart building systems, further accelerate adoption, positioning Asia-Pacific as the fastest-growing region in the global LED three-primary fluorescent light market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape is dominated by global lighting and LED technology companies with extensive R&D, distribution networks, and brand portfolios. Established players such as Signify N.V., OSRAM GmbH, General Electric Company, LEDVANCE GmbH, and Panasonic Corporation offer a range of three primary LED fluorescent products with high energy efficiency and color fidelity. Other significant competitors include Zumtobel Group AG, Acuity Brands, Inc., Eaton Corporation plc, and region specific manufacturers catering to localized demand. Competition focuses on product performance, color accuracy, integration with smart building systems, and cost efficiency. Strategic collaborations, acquisitions, and innovation in phosphor materials, semiconductor design, and digital controls help companies differentiate offerings.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary growth drivers are the global shift toward energy-efficient lighting and stringent government regulations banning inefficient traditional lamps. LED three-primary lights offer superior color rendering and longer lifespans compared to standard fluorescents. Increasing urbanization and the rapid expansion of smart building projects further stimulate demand for high-quality, sustainable illumination.

Q2. What are the main restraining factors for this market?

High initial installation costs compared to traditional lighting remain a significant restraint, particularly in price-sensitive developing regions. The market also faces challenges from the complexity of retrofitting existing infrastructure. Additionally, the availability of low-quality, inexpensive alternatives can dilute market value and decrease consumer trust in the performance of premium products.

Q3. Which segment is expected to witness high growth?

The LED Three Primary Fluorescent Fixtures segment is expected to witness the highest growth due to rising demand for integrated, energy-efficient lighting in commercial, industrial, and institutional spaces. Fixtures provide uniform illumination, easy installation, and compatibility with smart controls, driving adoption across offices, retail, and infrastructure modernization projects globally.

Q4. Who are the top major players for this market?

Leading companies in this space include Signify (formerly Philips Lighting), Osram, GE Lighting, and Panasonic Corporation. Other influential players include Cree LED, Zumtobel Group, and Acuity Brands. These organizations maintain their market position through continuous R&D, strategic acquisitions, and the development of specialized lighting solutions for industrial and professional applications.

Q5. Which country is the largest player?

China is the largest player in this market, serving as both the leading manufacturer and a massive consumer hub. The country benefits from a robust supply chain, significant government backing for energy-efficient technologies, and large-scale infrastructure development. Its dominance is supported by numerous domestic manufacturers producing components for both local and international markets.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model