Get Complete Analysis Of The Report - Download Updated Free Sample PDF

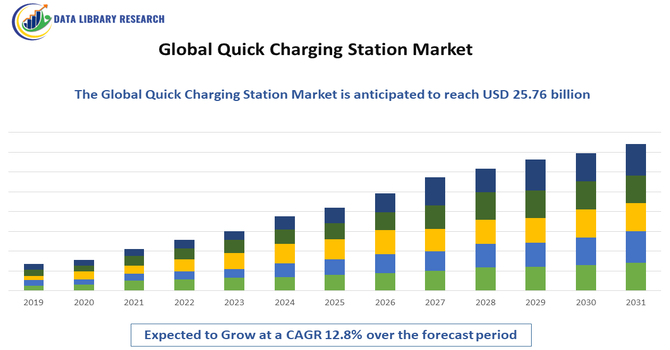

The Quick Charging Station Market refers to the global industry for high speed electric vehicle (EV) charging infrastructure that enables rapid replenishment of EV batteries in a short time, typically within 15–60 minutes or less. Quick chargers—often using DC fast charging technology—are essential to supporting long distance travel and reducing range anxiety among EV drivers. They are deployed in public locations, highways, commercial areas, fleets, and urban centers, connecting to smart grids and renewable energy sources. The demand is driven by the global shift to electrification, increasing EV adoption, and government incentives for clean mobility, accelerating investment in fast and ultra fast charging systems worldwide.

The Quick Charging Station Market is evolving rapidly with expansion of DC fast and ultra fast charging networks across key regions. Investment from automakers and infrastructure firms has accelerated deployment, with partnerships and electrification policies supporting growth. Standardization efforts—such as broader adoption of unified charging protocols—are improving interoperability and customer convenience. Smart charging features like dynamic load balancing, vehicle to grid integration, and real time data management are increasingly embedded, enhancing grid efficiency. Additionally, strategic placement of quick chargers along major highways and in urban mobility hubs supports long distance travel needs. Adoption is further fueled by advancements in battery technology that allow higher power transfer and reduced charging times.

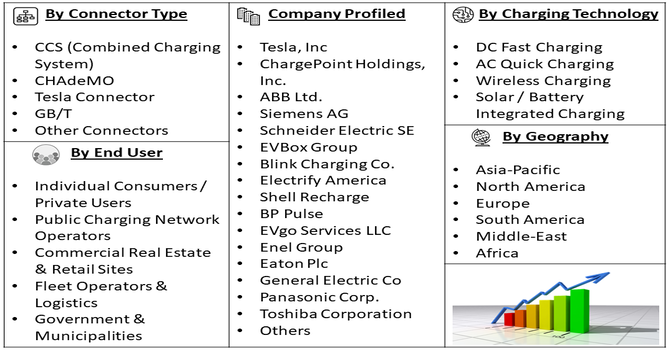

Segmentation: The Quick Charging Station Market is segmented by Charging Speed (Up to 50 kW (Fast Chargers), 51–150 kW (Rapid Chargers), 151–350 kW (Ultra fast Chargers) and Above 350 kW (Superfast / Megawatt Chargers)), Charging Technology (DC Fast Charging, AC Quick Charging, Wireless Charging and Solar / Battery Integrated Charging), Connector Type (CCS (Combined Charging System), CHAdeMO, Tesla Connector, GB/T and Other Connectors), Installation Location (Residential Charging Stations, Commercial Charging Stations, Highway / Roadside Charging Stations and Public Parking Facilities), End User (Individual Consumers / Private Users, Public Charging Network Operators, Commercial Real Estate & Retail Sites, Fleet Operators & Logistics and Government & Municipalities), Power Source (Grid Connected Stations, Solar Powered / Renewable Source Charging and Battery Storage Integrated Stations ), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The primary drivers of the Quick Charging Station Market is the rapid global adoption of electric vehicles (EVs).

Governments across major economies are implementing stringent emissions regulations, offering incentives, and setting ambitious EV adoption targets, prompting consumers and fleets to transition to electric mobility. For instance, in 2025, NITI Aayog released the report “Unlocking a USD 200 Billion Opportunity: Electric Vehicles in India”, highlighting strategies to accelerate India’s electric mobility transition. Its insights supported policy development and infrastructure expansion, contributing to the rapid global adoption of EVs and stimulating growth in the global quick charging station market.

As EV sales increase, demand for fast and reliable charging infrastructure grows, particularly those offering quick charging that supports long distance travel and reduces range anxiety. Automakers are also increasingly integrating fast charging capabilities into vehicle designs, further fueling the need for robust charging networks. This rising EV penetration creates significant investment opportunities and accelerates the expansion of quick charging infrastructure worldwide.

Technological innovation is a key driver for the Quick Charging Station Market. Advances in power electronics, cooling systems, and battery management have enabled higher output charging stations that can significantly reduce charging times.

Integration of smart grid features facilitates efficient load management, while AI and digital platforms optimize station uptime and user experience. For instance, in 2023, Lotus introduced its ultra-fast 450 kW DC charger and modular multi-vehicle charging units, addressing charging anxiety—a key barrier for nearly 80% of potential EV buyers. This technological advancement enhanced reliability and accessibility, boosting consumer confidence and driving growth in the global quick charging station market through innovative high-speed infrastructure deployment.

Partnerships between charging network operators, automakers, and energy providers are accelerating R&D in ultra fast charging solutions. In addition, improved interoperability standards allow broader compatibility between EV models and charging infrastructure. These technological developments enhance reliability, convenience, and scalability of fast charging networks, driving broader consumer adoption and infrastructure deployment globally.

Market Restraints:

A major restraint facing the Quick Charging Station Market is the high infrastructure and deployment cost. Quick and ultra fast charging stations require substantial capital expenditure for high power electrical equipment, grid upgrades, and site development. Costs are further increased by the need for robust back end software, payment systems, and ongoing maintenance. Additionally, grid capacity limitations in certain regions necessitate expensive upgrades to support high power output, leading to longer project timelines. These financial barriers can deter investment, particularly in developing markets or lower density areas where return on investment is uncertain. The high cost of installation and operation slows infrastructure rollout compared with lower speed charging alternatives.

The Quick Charging Station Market significantly influences socioeconomic development by enabling broader EV adoption, reducing greenhouse gas emissions, and supporting energy transition goals. By reducing charging times and expanding access, quick chargers make EVs more practical for daily use and long distance travel, increasing consumer confidence. Infrastructure investments create jobs in manufacturing, installation, operations, and maintenance while boosting local economies. The deployment of charging stations also stimulates tourism, retail footfall, and commercial activity at charging locations. Additionally, growth in electrification reduces dependency on fossil fuels, lowers transportation costs for consumers, and aligns with national environmental policies, contributing to cleaner urban air quality and sustainable mobility ecosystems.

Segmental Analysis:

The 51–150 kW rapid chargers segment is expected to witness the highest growth over the forecast period due to its balance of fast charging capability and cost-effectiveness. These chargers significantly reduce vehicle downtime for private EV owners, fleet operators, and public charging networks without requiring the high infrastructure costs associated with ultra-fast chargers. Rapid chargers are increasingly installed in urban centers, highways, and commercial hubs to meet growing EV adoption. Compatibility with a wide range of vehicles, ease of integration with smart grid systems, and government incentives for mid-power charging infrastructure further propel adoption, making this segment a key driver of global market expansion.

The DC fast charging segment is projected to witness the highest growth due to its ability to deliver high-voltage direct current directly to EV batteries, reducing charging times to 15–60 minutes. DC fast chargers are critical for long-distance travel, commercial fleets, and public charging networks, making them increasingly preferred over AC chargers. The segment benefits from technological advancements in power electronics, improved battery compatibility, and smart grid integration. Growing EV sales, government incentives, and expansion of highway charging networks support widespread deployment. The convenience and reliability of DC fast chargers make them the backbone of modern EV infrastructure, boosting adoption globally.

The Tesla connector segment is expected to witness the highest growth as Tesla’s EV popularity continues to expand globally. Tesla Superchargers and connector standards enable high-speed charging specifically designed for Tesla vehicles, ensuring safety, efficiency, and compatibility. Expansion of Tesla’s Supercharger network in North America, Europe, and Asia-Pacific increases the accessibility of rapid charging for private and fleet users. Integration with smart charging features, mobile apps, and seamless billing enhances user experience. Tesla’s brand loyalty, combined with rising EV adoption and cross-compatibility initiatives for other EVs, drives growth. This segment’s expansion contributes significantly to the overall development of the quick charging station market.

The commercial charging stations segment is projected to witness the highest growth due to increasing demand from businesses, fleet operators, and public facility operators seeking to provide convenient EV charging for employees, customers, and visitors. Commercial stations are strategically installed in office complexes, logistics hubs, and public spaces, often equipped with rapid and ultra-fast chargers to support high traffic volumes. Growing EV adoption among company fleets and the need to reduce emissions in corporate operations drive investments in commercial charging infrastructure. Government incentives, smart grid integration, and energy management solutions further enhance deployment. The segment’s growth underlines the commercialization and monetization potential of fast charging infrastructure.

The commercial real estate & retail sites segment is expected to witness the highest growth as property owners increasingly install EV chargers to attract customers and tenants. Retail chains, shopping malls, and office complexes deploy rapid chargers to provide added convenience, promote sustainability, and enhance foot traffic. Integration with renewable energy sources, smart billing systems, and loyalty programs improves customer engagement. Incentives from governments and utilities further motivate property developers to adopt EV infrastructure. As EV ownership grows, these sites serve as strategic charging hubs, offering mid-to-rapid charging solutions while generating additional revenue streams, making this segment critical in the overall market expansion.

The solar powered / renewable source charging segment is projected to witness the highest growth due to increasing emphasis on sustainability and reduced grid dependency. Integrating solar panels or renewable energy systems with fast chargers minimizes operational costs, lowers carbon emissions, and enhances energy resilience. These stations appeal to environmentally conscious consumers, businesses, and government initiatives promoting green mobility. Technological advancements in energy storage and smart grid integration allow efficient load management and peak shaving. Rising EV adoption and supportive renewable energy policies globally further boost deployment. Solar-powered charging stations are becoming key components of sustainable EV infrastructure, driving both environmental and economic benefits in the market.

The Asia-Pacific region is expected to witness the highest growth over the forecast period due to rapid EV adoption, supportive government policies, and urbanization trends in China, India, Japan, and Southeast Asia.

Massive investments in charging infrastructure, public-private partnerships, and subsidies for fast chargers are accelerating market expansion. For instance, in December 2025, Ministry of Heavy Industries, reported that over the past five years, India installed 29,151 EV charging stations, including 8,805 fast chargers, supported by FAME-I, FAME-II, and the PM E-DRIVE Scheme. These developments accelerated private investment and infrastructure expansion, strengthening the Asia-Pacific quick charging station market and driving adoption of rapid and ultra-fast EV charging networks across the region.

Increasing demand for long-distance travel, logistics electrification, and smart city initiatives fuels deployment of rapid and ultra-fast charging stations. Technological innovation, such as DC fast chargers and solar-powered stations, further supports adoption. Rising disposable incomes, growing awareness of environmental sustainability, and expanding automotive manufacturing hubs make Asia-Pacific the fastest-growing region in the global quick charging station market.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Quick Charging Station Market includes major diversified energy, automotive, and infrastructure companies alongside specialized charging network operators. Established players such as Tesla, Inc. and ChargePoint Holdings, Inc. leverage global networks and technology innovation to maintain strong market share. Traditional industrial giants like ABB Ltd. and Siemens AG compete by offering high power charging platforms and grid integration solutions. Regional operators and emerging brands focus on niche markets and local expansion. Competition is driven by rapid technological advancements, strategic partnerships with automakers, investment in ultra fast chargers, and software capabilities that enhance user experience and network management.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

Rapid electric vehicle (EV) adoption and government subsidies for green infrastructure are the primary drivers. Stringent emission regulations and the expansion of long-distance travel capabilities necessitate faster charging solutions. Additionally, technological advancements in battery chemistry and power electronics allow for higher power outputs, significantly reducing downtime and improving consumer convenience.

Q2. What are the main restraining factors for this market?

The high initial cost of installing DC fast-charging hardware and necessary grid upgrades remains a significant barrier. Compatibility issues between different charging standards (CCS, CHAdeMO, and NACS) can create consumer confusion. Furthermore, the strain on aging electrical grids and the slow pace of permitting processes often delay the deployment of new stations.

Q3. Who are the top major players for this market?

Key industry leaders include ABB Ltd, Tesla (with its Supercharger network), Siemens AG, and Schneider Electric. Other significant contributors include ChargePoint, Tritium, and EVgo. These companies focus on strategic partnerships with automakers and utility providers to expand their networks and develop modular, scalable charging solutions for diverse global environments.

Q4. Which country is the largest player?

China is currently the largest player in the quick charging station market. The country boasts the world’s most extensive public charging network, supported by aggressive state-led investment and a massive domestic EV manufacturing base. Its focus on standardized infrastructure and urban density has allowed it to outpace North America and Europe.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model