Get Complete Analysis Of The Report - Download Updated Free Sample PDF

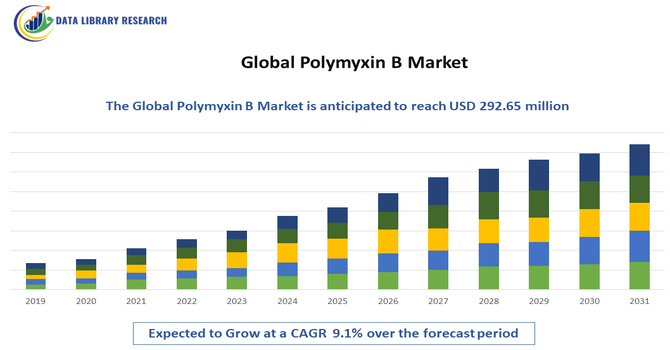

The Global Polymyxin B Market refers to the worldwide production, distribution, and commercialization of Polymyxin B–based antibiotic formulations used to treat severe Gram-negative bacterial infections. Polymyxin B is a last-resort antimicrobial agent primarily administered intravenously or topically for multidrug-resistant (MDR) infections, including those caused by Pseudomonas aeruginosa, Acinetobacter baumannii, and Klebsiella pneumoniae. The market includes active pharmaceutical ingredient (API) manufacturers, finished dosage producers, hospital procurement networks, and distributors. Growth is influenced by rising antimicrobial resistance (AMR), increasing hospital-acquired infections (HAIs), expanding critical care infrastructure, and renewed clinical reliance on older antibiotics due to limited novel antimicrobial development pipelines worldwide.

The key market trends include increasing clinical reliance on Polymyxin B as carbapenem resistance rises globally. Hospitals are updating antimicrobial stewardship protocols to optimize dosing strategies and minimize nephrotoxicity risks. Combination therapies involving Polymyxin B with other antibiotics are gaining attention to enhance efficacy against MDR pathogens. Emerging markets are witnessing higher demand due to expanding intensive care units and improved diagnostic capabilities. Additionally, regulatory agencies are encouraging responsible antibiotic use while supporting research into safer polymyxin formulations. Growth in injectable generics manufacturing and hospital procurement contracts further shapes the competitive landscape, as affordability and supply chain reliability become increasingly important purchasing criteria.

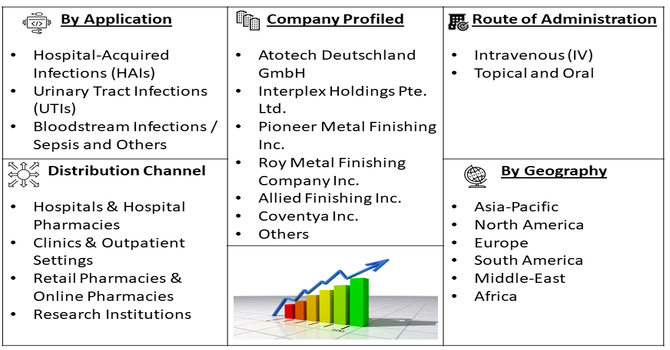

Segmentation: The Global Polymyxin B Market is segmented by Product (Injectable Formulations, Topical Formulations, Ophthalmic Formulations and Other Advanced Formulations), Application (Hospital-Acquired Infections (HAIs), Urinary Tract Infections (UTIs), Bloodstream Infections / Sepsis and Others), Distribution Channel (Hospitals & Hospital Pharmacies, Clinics & Outpatient Settings, Retail Pharmacies & Online Pharmacies, and Research Institutions), Route of Administration (Intravenous (IV), Topical and Oral), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

A primary driver of the global Polymyxin B market is the rapid rise of antimicrobial resistance worldwide. Increasing resistance to carbapenems and other broad-spectrum antibiotics has revived the clinical importance of polymyxins as last-line therapies. Healthcare providers increasingly rely on Polymyxin B to manage severe infections caused by multidrug-resistant Gram-negative bacteria, particularly in intensive care settings. Growing surveillance data highlighting resistant strains have reinforced demand across developed and emerging economies. As hospital-acquired infections continue to rise and therapeutic alternatives remain limited, Polymyxin B has regained strategic importance in infectious disease treatment protocols, driving consistent demand growth across critical care environments.

Another key driver is the global expansion of hospital infrastructure and intensive care capacity. Increasing numbers of complex surgeries, organ transplants, cancer therapies, and invasive procedures have elevated infection risks, necessitating reliable access to potent antibiotics.

In December 2025, The U.S. signed USD 2.3 billion in MOUs with Madagascar, Sierra Leone, Botswana, and Ethiopia, driving expansion of critical care and hospital infrastructure while boosting investments in infectious disease management. These agreements strengthened global preparedness, supported local healthcare capacity, and indirectly stimulated the Polymyxin B market by increasing demand for therapies targeting multidrug-resistant infections.

Emerging economies are investing heavily in healthcare modernization, leading to greater antibiotic procurement volumes. Improved diagnostic technologies also enable faster identification of resistant pathogens, prompting timely Polymyxin B administration. As healthcare systems strengthen critical care capabilities, demand for effective last-resort antibiotics grows. This structural expansion in healthcare delivery systems significantly supports long-term market growth for Polymyxin B products worldwide.

Market Restraints:

A major restraint in the global Polymyxin B market is the risk of nephrotoxicity and neurotoxicity associated with its use. Because Polymyxin B is often administered in critically ill patients, monitoring kidney function is essential, increasing clinical complexity and cost. Concerns about adverse effects may limit widespread adoption and encourage physicians to consider alternative treatments where available. Strict antimicrobial stewardship programs also aim to restrict unnecessary use to prevent further resistance development. Additionally, regulatory scrutiny regarding dosing guidelines and safety labeling can influence prescribing patterns. These safety considerations act as a moderating factor on overall market expansion.

The Polymyxin B market has significant socioeconomic implications due to its critical role in combating life-threatening drug-resistant infections. Effective treatment of MDR infections reduces mortality, shortens hospital stays, and lowers long-term healthcare costs associated with complications. However, increased reliance on last-resort antibiotics reflects broader antimicrobial resistance challenges, which strain healthcare budgets and public health systems. In low- and middle-income countries, access to affordable injectable antibiotics can improve survival rates in intensive care units. Simultaneously, the need for careful monitoring of adverse effects requires additional clinical resources. Thus, Polymyxin B remains essential in sustaining effective infectious disease management globally.

Segmental Analysis:

The topical formulations segment of the Polymyxin B market is expected to witness the highest growth over the forecast period due to rising cases of skin and soft tissue infections, burns, and post-surgical wound complications. Increasing awareness about localized antibiotic therapy, which minimizes systemic toxicity risks associated with polymyxins, is supporting demand. Growth in outpatient care, dermatology clinics, and over-the-counter combination antibiotic products further accelerates segment expansion. Additionally, the growing elderly population and diabetic patients prone to wound infections are contributing to sustained adoption of topical Polymyxin B formulations globally.

The urinary tract infections (UTIs) segment is projected to record the fastest growth in the Polymyxin B market due to the increasing prevalence of multidrug-resistant Gram-negative pathogens. Rising antibiotic resistance in recurrent and complicated UTIs has strengthened reliance on last-line therapies such as Polymyxin B. The growing geriatric population, higher incidence of catheter-associated infections, and expanding hospital admissions further support demand. In addition, improved diagnostic capabilities and antimicrobial stewardship programs are promoting targeted therapy, driving the adoption of Polymyxin B in severe and resistant UTI cases worldwide.

Hospitals and hospital pharmacies are anticipated to witness the highest growth in the Polymyxin B market owing to the increasing burden of hospital-acquired infections (HAIs) and critical care admissions. As Polymyxin B is primarily administered for severe multidrug-resistant infections, its usage remains concentrated in intensive care units and tertiary care settings. Growing investments in hospital infrastructure, particularly in emerging economies, and the expansion of antimicrobial stewardship programs are reinforcing demand. Moreover, centralized procurement systems in hospitals ensure steady supply and higher volume utilization, strengthening this segment’s growth trajectory.

The intravenous (IV) segment is expected to register the highest growth over the forecast period due to its essential role in treating life-threatening systemic infections such as sepsis and bloodstream infections. IV administration ensures rapid drug delivery and optimal therapeutic concentration, which is critical in critical care settings. The increasing incidence of carbapenem-resistant infections and rising ICU admissions globally are major growth drivers. Furthermore, advancements in infusion technologies and improved dosing protocols to manage nephrotoxicity risks are encouraging broader clinical adoption of intravenous Polymyxin B therapy.

North America is projected to experience the highest growth in the Polymyxin B market, supported by advanced healthcare infrastructure, strong surveillance systems, and high awareness regarding antimicrobial resistance. For instance, in 2025, Venus Remedies’ VRP-034 received QIDP designation from the US FDA, highlighting its novel supramolecular polymyxin B formulation with reduced nephrotoxicity. This milestone accelerated regulatory incentives, enhanced development prospects, and strengthened North America’s Polymyxin B market by expanding safer treatment options for bloodstream infections and addressing growing antimicrobial resistance challenges.

The region faces a significant burden of multidrug-resistant infections, prompting the use of last-line antibiotics. Favorable reimbursement policies, well-established hospital networks, and ongoing research activities further contribute to market expansion.

Additionally, increasing investments in infectious disease management and government initiatives aimed at combating antibiotic resistance are expected to drive sustained demand for Polymyxin B across the region. For instace, in January 2026, USD 60 million Gr-ADI funding by the Gates Foundation, Novo Nordisk Foundation, and Wellcome boosted global investments in infectious disease research, emphasizing Gram-negative antibiotic discovery. This initiative accelerated innovation, supported novel therapies, and indirectly strengthened North America’s Polymyxin B market by fostering development of new treatments to combat multidrug-resistant infections and antimicrobial resistance.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the global Polymyxin B market is characterized by a mix of multinational pharmaceutical companies and regional generic drug manufacturers. Competition primarily centers on pricing, regulatory compliance, manufacturing quality standards, and supply reliability. Many players operate in the injectable generics segment, supplying hospitals through tender-based procurement systems. Companies invest in improving production efficiency and ensuring adherence to Good Manufacturing Practices (GMP) to maintain market credibility. Strategic partnerships with healthcare institutions and distributors support geographic expansion. While innovation in polymyxin derivatives is limited, differentiation occurs through formulation improvements, combination therapies, and enhanced pharmacovigilance initiatives to ensure patient safety.

The major players for this market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The primary driver is the alarming rise in multi-drug resistant (MDR) Gram-negative bacterial infections, particularly "superbugs" like carbapenem-resistant Enterobacteriaceae. As traditional antibiotics fail, Polymyxin B is increasingly used as a last-resort treatment. Furthermore, increased healthcare spending and improved diagnostic capabilities in emerging economies are significantly boosting global market demand.

Q2. What are the main restraining factors for this market?

The significant risk of nephrotoxicity and neurotoxicity remains a major restraint, leading clinicians to limit usage to extreme cases. Additionally, the emergence of Polymyxin-resistant strains, often mediated by the mcr-1 gene, threatens long-term efficacy. High costs of specialized parenteral administration and stringent regulatory approval processes also hinder broader adoption.

Q3. Which segment is expected to witness high growth?

The parenteral (injectable) administration segment is expected to witness the highest growth. This is due to the rising incidence of severe systemic infections, such as sepsis and hospital-acquired pneumonia, which require rapid intravenous intervention. The hospital pharmacy distribution channel similarly sees high growth as these drugs are primarily administered inpatient.

Q4. Who are the top major players for this market?

The market is dominated by established pharmaceutical giants and specialized generic manufacturers. Key players include Pfizer Inc., Eurofarma Laboratórios, Xellia Pharmaceuticals, and Gland Pharma Limited. Other significant contributors include Fresenius Kabi, Lupin Pharmaceuticals, and various regional manufacturers in India and China focusing on affordable high-quality generic antibiotic production.

Q5. Which country is the largest player?

The United States is currently the largest player in the Polymyxin B market. This dominance is attributed to a sophisticated healthcare infrastructure, high awareness of antimicrobial resistance, and the presence of major pharmaceutical innovators. Furthermore, rigorous clinical guidelines in the U.S. often prioritize the use of these last-line therapies.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model