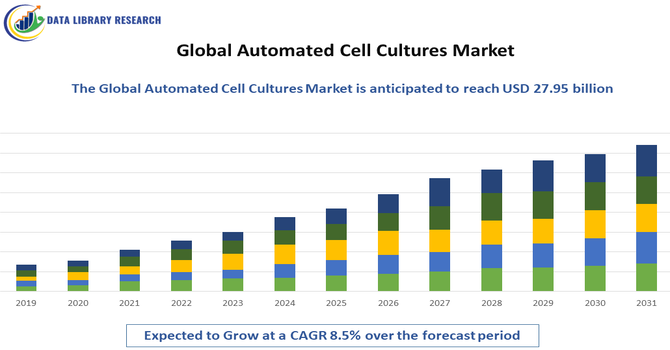

The Global Automated Cell Cultures Market was valued at USD 14.13 billion in 2026 and is expected to reach USD 27.95 billion by 2033, growing at a CAGR of 8.5% from 2026-2033.

Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Automated Cell Cultures Market refers to the industry focused on developing and providing automated systems and technologies for culturing cells in laboratories and biomanufacturing. These systems streamline cell growth, monitoring, and maintenance, reducing manual labor and minimizing contamination risks. Automated cell culture solutions enhance reproducibility, scalability, and efficiency in research, drug development, regenerative medicine, and biopharmaceutical production. Growth in this market is driven by increasing demand for advanced cell therapies, rising investments in biotechnology, and the need for high-throughput screening and personalized medicine.

The Global Automated Cell Cultures Market is driven by rising adoption of automation in research and biomanufacturing to improve efficiency, scalability, and reproducibility. Advances in robotic systems, bioreactors, and AI-enabled monitoring tools are enabling precise control over cell growth and differentiation. High-throughput screening, personalized medicine, and regenerative therapies are increasingly relying on automated systems to reduce contamination risks and labor costs. Integration with digital platforms and data analytics supports real-time monitoring and process optimization.

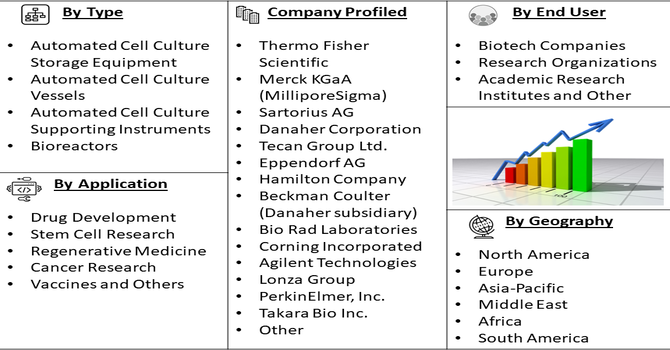

Segmentation: The Global Automated Cell Cultures Market is segmented by Products (Instruments, Reagents and Kits, and Others), Type (Automated Cell Culture Storage Equipment, Automated Cell Culture Vessels, Automated Cell Culture Supporting Instruments, Bioreactors), Application (Drug Development, Stem Cell Research, Regenerative Medicine, Cancer Research, Vaccines, and Others), End User (Biotech Companies, Research Organizations, Academic Research Institutes, and Other) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The growing demand for cell-based therapies, including stem cell treatments, CAR-T therapies, and regenerative medicine, is a primary driver for the automated cell cultures market. Traditional manual cell culture methods are labor-intensive, prone to contamination, and limited in scalability. Automated systems provide standardized, reproducible conditions, enabling the production of large volumes of high-quality cells for clinical and research applications. As the biotechnology and pharmaceutical industries expand their pipelines for personalized therapies and advanced biologics, the need for reliable, scalable, and precise automated cell culture solutions continues to accelerate globally.

Rapid technological advancements, such as robotic arms, automated bioreactors, AI-enabled monitoring, and real-time analytics, are driving market growth. High-throughput automated systems allow simultaneous cultivation of multiple cell lines under controlled conditions, improving efficiency, reducing human error, and enhancing reproducibility.

In May 2024, SINFONIA TECHNOLOGY delivered CellQualia ICP systems to Keio University, completing performance qualification in April. These systems enhanced technological advancements and high-throughput automation by enabling stable, efficient production of high-quality cell medicines, while supporting automated storage and streamlined handling in regenerative medicine applications. Integration with laboratory information management systems (LIMS) and cloud-based analytics supports data-driven process optimization and quality control. Pharmaceutical companies, academic institutions, and contract research organizations increasingly adopt these technologies to accelerate drug discovery, toxicity testing, and vaccine development, further boosting demand for automated cell culture solutions worldwide.

Market Restraints:

A significant restraint for the automated cell culture market is the high initial capital investment and ongoing maintenance costs associated with these systems. Advanced bioreactors, robotic platforms, and monitoring software require substantial funding, making adoption challenging for small laboratories and emerging biotech companies. Additionally, maintenance, calibration, and specialized training for personnel add to operational expenses. Budget constraints can delay deployment and limit scalability in certain regions. Regulatory compliance, validation, and integration with existing laboratory infrastructure further increase costs, restraining widespread adoption despite the efficiency, reproducibility, and quality benefits offered by automated cell culture technologies.

Automated cell culture technologies have significant socioeconomic benefits by accelerating drug development, supporting regenerative medicine, and improving healthcare outcomes. They reduce labor intensity and contamination risks, lowering research and production costs, which enhances the affordability of therapies. Increased efficiency in biopharmaceutical manufacturing leads to faster delivery of treatments to patients, contributing to public health improvements. Additionally, automation stimulates job creation in high-skill roles such as bioinformatics, robotics maintenance, and process engineering, while upskilling the workforce. Widespread adoption in research institutions and hospitals helps bridge healthcare gaps, making advanced therapies and diagnostics more accessible and improving quality of life globally.

Segmental Analysis:

The reagents and kits segment is expected to witness the highest growth over the forecast period due to rising demand for standardized, ready-to-use solutions that simplify automated cell culture processes. These products reduce manual preparation, minimize contamination risk, and ensure consistent cell growth and quality. Pharmaceutical, biotechnology, and academic research laboratories increasingly rely on pre-formulated reagents, growth media, and assay kits to accelerate experimentation and therapeutic development. Integration with automated platforms further enhances throughput and reproducibility. As cell-based research and regenerative medicine expand, the demand for high-quality, reliable reagents and kits is projected to drive significant market growth globally.

The automated cell culture storage equipment segment is expected to grow rapidly, driven by the need for secure, scalable, and temperature-controlled storage of cell lines and cultures. Biorepositories, research laboratories, and biopharmaceutical companies require automated storage systems that integrate with cell culture platforms to preserve cell viability, reduce human error, and streamline retrieval. Advanced systems offer real-time monitoring, alarm notifications, and data logging to ensure compliance with regulatory standards. The growth of stem cell therapies, regenerative medicine, and biopharmaceutical production is further accelerating the adoption of automated storage solutions, making this segment a key contributor to overall market expansion.

The drug development segment is expected to witness the highest growth, driven by increasing demand for high-throughput, reproducible, and scalable cell culture systems in pharmaceutical research. Automated cell cultures enable efficient screening of compounds, toxicity testing, and preclinical validation, significantly reducing development timelines. Integration with AI, machine learning, and predictive analytics enhances decision-making and accelerates the identification of promising drug candidates. As pharmaceutical companies invest in biologics, vaccines, and personalized medicines, automated cell culture platforms play a crucial role in reducing costs, improving productivity, and ensuring consistent quality, positioning the drug development segment as a key growth driver.

The biotech companies segment is projected to experience the highest growth over the forecast period, driven by increased research and therapeutic development activities. Biotech firms are leveraging automated cell culture systems to accelerate drug discovery, regenerative medicine, and cell therapy manufacturing. Automation ensures reproducibility, scalability, and compliance with regulatory standards, enabling companies to meet growing demand for biologics and personalized therapies. Rising investment in biotechnology, coupled with the expansion of contract research and manufacturing services, has further fueled adoption. As biotech companies seek cost-effective, high-throughput solutions, automated cell culture technologies have become central to innovation and market competitiveness.

North America is expected to witness the highest growth over the forecast period, supported by advanced R&D infrastructure, early adoption of automation technologies, and substantial investments in biotechnology and pharmaceuticals.

The U.S. and Canada lead in cell therapy, regenerative medicine, and biologics production, creating strong demand for automated cell culture platforms. For instance, in 2025, BD and Opentrons Labworks announced a multi-year collaboration to integrate robotic liquid-handling into BD’s single-cell multiomics instruments. This partnership automated critical experimental steps, enhancing efficiency and scalability in disease research and drug development. It positively impacted North America’s Automated Cell Cultures Market by driving adoption of high-throughput, automated systems and accelerating advancements in cell-based research and therapeutic development.

Regulatory support, availability of skilled workforce, and integration with AI, robotics, and cloud-based monitoring systems further drive adoption. Increasing collaborations between academic institutions, biotech firms, and pharmaceutical companies enhance innovation. As a result, North America remains a dominant and rapidly growing region for automated cell culture solutions, reflecting robust market potential and technological leadership.

| Report Matrics | Details |

| Market Size Value | USD 27.95 billion |

| Growth Rate | CAGR of 8.5 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months' analysis support) |

| To Learn More About This Report | Request a Free Sample Copy |

The competitive landscape of the Global Automated Cell Cultures Market is highly dynamic, with established biotechnology firms, laboratory equipment manufacturers, and emerging startups competing on innovation, efficiency, and system integration. Major players focus on developing robotic platforms, automated bioreactors, and software for real-time monitoring and process control. Strategic collaborations, acquisitions, and partnerships are common to expand product portfolios, enter new geographic markets, and integrate AI and IoT capabilities. Companies differentiate through scalability, customization, ease of use, and compliance with regulatory standards. Continuous R&D investment and technological innovation are key to gaining a competitive edge and meeting growing demand in research and biomanufacturing sectors.

The major players for above market are:

Recent Development

Q1. What are the main growth-driving factors for this market?

The market is driven by the rising demand for biopharmaceuticals and monoclonal antibodies, which require precise, large-scale cell production. Automation minimizes human error and contamination risks, ensuring high-quality yields. Additionally, increased funding for regenerative medicine and the move toward high-throughput screening in drug discovery are significantly boosting adoption rates.

Q2. What are the main restraining factors for this market?

High capital investment for automated systems and specialized infrastructure remains a primary barrier, particularly for smaller research labs. The complexity of integrating automation with existing workflows and the need for highly skilled personnel to operate these systems also slow market expansion. Furthermore, stringent regulatory approval processes can delay product launches.

Q3. Which segment is expected to witness high growth?

The Automated Cell Culture Storage Equipment segment grew due to rising demand for secure, scalable, and temperature-controlled storage solutions. Integration with automated platforms ensured cell viability, reduced human error, and streamlined retrieval. Expansion in stem cell therapies, regenerative medicine, and biopharmaceutical production further accelerated adoption, driving market growth globally.

Q4. Who are the top major players for this market?

Key industry leaders include Thermo Fisher Scientific, Danaher Corporation (through Beckman Coulter and Cytiva), Sartorius AG, and Merck KGaA. Other significant players like Lonza, Eppendorf, and Tecan Group contribute through innovative robotic platforms and bioreactor technologies. these companies focus on strategic acquisitions and R&D to maintain their competitive edge.

Q5. Which country is the largest player?

The United States is the largest player in the global market, fueled by a robust biotechnology sector and extensive pharmaceutical R&D spending. The presence of major industry players, coupled with advanced healthcare infrastructure and favorable government initiatives for stem cell research, ensures its continued dominance in the automated cell culture landscape.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model