Get Complete Analysis Of The Report - Download Updated Free Sample PDF

The Global Intestinal Dysmotility Therapy Market encompasses the development, production, and commercialization of treatments for gastrointestinal motility disorders, including gastroparesis, chronic intestinal pseudo-obstruction, and irritable bowel syndrome. The market features a diverse range of therapies, such as prokinetic agents, neuromodulators, and advanced diagnostic tools. Rising prevalence of motility disorders, growing awareness among healthcare providers, and technological innovations in drug delivery and personalized medicine are driving market growth and expanding treatment options worldwide. The global intestinal dysmotility therapy market is a specialized segment within the broader gastrointestinal therapeutics landscape, focusing on disorders characterized by impaired motility of the intestines. These conditions, including chronic constipation, gastroparesis, and intestinal pseudo-obstruction, significantly impact patients' quality of life and present substantial clinical challenges. The market is driven by factors such as the increasing prevalence of gastrointestinal disorders, advancements in diagnostic technologies, and the development of novel therapeutic agents.

The is witnessing several notable trends that are shaping its growth and evolution. There is a strong shift toward personalized and precision medicine, where treatment plans are tailored to individual patients based on their specific symptoms and underlying causes, improving efficacy and minimizing side effects. The integration of artificial intelligence (AI) and machine learning (ML) is enhancing diagnostic accuracy and predicting treatment responses, enabling more personalized therapy regimens. Advancements in diagnostic techniques, such as high-resolution manometry and advanced imaging, allow for earlier and more accurate detection of gastrointestinal motility disorders. Additionally, the market is seeing the emergence of novel therapeutic agents, including new prokinetic drugs, neuromodulators, and biologics that target specific motility pathways. The adoption of telemedicine and remote monitoring is expanding access to care, particularly for patients in remote regions or requiring long-term management.

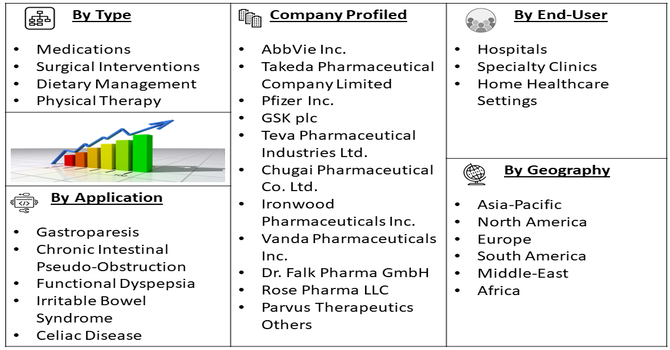

Segmentation: Global Intestinal Dysmotility Therapy Market is segmented By Therapy Type (Medications, Surgical Interventions, Dietary Management, Physical Therapy), Disease Indication (Gastroparesis, Chronic Intestinal Pseudo-Obstruction, Functional Dyspepsia, Irritable Bowel Syndrome, Celiac Disease), End-User (Hospitals, Specialty Clinics, Home Healthcare Settings), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The increasing incidence of conditions such as gastroparesis, chronic intestinal pseudo-obstruction (CIPO), and irritable bowel syndrome (IBS) is a major driver for the market. As these disorders become more common globally, there is growing demand for effective therapies that manage symptoms, improve gastrointestinal motility, and enhance patient quality of life, fueling the adoption of advanced intestinal dysmotility treatments. In 2024, The American Journal of Gastroenterology reported that a comprehensive analysis of 96 studies across 51 countries reported that irritable bowel syndrome (IBS) had an overall prevalence of 14%, higher than previous estimates of 11.2%. Using the Rome IV criteria, prevalence was notably higher despite its stricter definition. The mixed subtype (IBS-M) was generally more common than diarrhea-predominant (IBS-D) and constipation-predominant (IBS-C), although IBS-C exceeded IBS-D under Rome IV. The United Kingdom accounted for the highest proportion of global cases at 67.5%, with women slightly more affected than men. These findings underscored the rising burden of gastrointestinal disorders, driving increased demand for effective therapies and accelerating growth in the Global Intestinal Dysmotility Therapy Market.

Innovations in prokinetic drugs, neuromodulators, biologics, and surgical interventions, along with improvements in diagnostic tools such as high-resolution manometry and advanced imaging techniques, are driving market growth. These advancements enable earlier and more accurate diagnosis, more effective treatment options, and better patient outcomes, encouraging healthcare providers to adopt newer intestinal dysmotility therapies. In August 2021, an article published by journal, Sec. Gastrointestinal and Hepatic Pharmacology, reported that that prokinetic agents and emerging pharmacological therapies effectively improved gastric motility and alleviated gastroparesis symptoms, with several novel agents targeting diverse motor and cellular pathways showing promise. These advancements enhanced understanding of disease mechanisms and informed the development of more precise, effective treatments. Consequently, they positively impacted innovations in therapeutic and diagnostic technologies, driving growth in the Intestinal Dysmotility Therapy Market.

Market Restraints:

High treatment costs associated with advanced medications, surgical interventions, and specialized therapies can limit patient access, particularly in emerging economies. Complexity in diagnosis of intestinal dysmotility disorders, due to overlapping symptoms with other gastrointestinal conditions, often leads to delayed or inaccurate treatment, hindering market expansion. Additionally, the limited availability of highly effective therapies for certain subtypes of dysmotility and the need for long-term management can reduce patient adherence and slow adoption rates. Regulatory challenges and the requirement for specialized healthcare professionals to administer treatments further constrain market growth.

The Global Intestinal Dysmotility Therapy Market has considerable socio-economic implications by addressing disorders that significantly impair gastrointestinal function and patients’ quality of life. Effective therapies reduce hospitalization rates, medical costs, and productivity losses associated with chronic dysmotility conditions, easing the financial burden on healthcare systems and patients. The market stimulates economic growth by driving investments in research, development, and commercialization of innovative treatments, while generating employment across pharmaceutical, biotechnology, and healthcare sectors. Additionally, improved patient outcomes enhance social well-being, enabling affected individuals to maintain daily activities and workforce participation. Government initiatives supporting access to advanced therapies further strengthen healthcare infrastructure. Thus, the market contributes to both economic advancement and societal health improvement worldwide.

Segmental Analysis:

The medications segment is expected to witness the highest growth within the therapy type category. Medications, including prokinetic agents, neuromodulators, and anti-inflammatory drugs, are widely used to manage intestinal dysmotility symptoms and improve gastrointestinal motility. Their non-invasive nature, ease of administration, and ability to provide symptom relief make them the most preferred treatment option among patients and healthcare providers. Advances in pharmaceutical formulations are also enhancing their efficacy and safety, contributing to the growth of this segment.

Gastroparesis is projected to dominate the disease indication segment. Characterized by delayed gastric emptying without mechanical obstruction, gastroparesis significantly affects patients’ quality of life and requires long-term management. The rising prevalence of gastroparesis, along with growing awareness among physicians and patients about available therapies, is driving demand for effective treatment options in this segment. The market for pharmacological therapies, including prokinetic agents, antiemetics, and novel biologics, is expected to witness significant growth. Increasing investment in drug development, coupled with advancements in diagnostic technologies for early detection, is expanding treatment accessibility. Additionally, the rising adoption of combination therapies and personalized treatment approaches is improving patient outcomes and adherence. As a result, pharmaceutical companies are focusing on innovative formulations and targeted therapies, which are further fueling market expansion. Growing healthcare infrastructure, insurance coverage, and government support for chronic gastrointestinal disorders are also contributing to the steady rise in demand for intestinal dysmotility therapies globally.

Hospitals represent the largest end-user segment due to their comprehensive diagnostic and therapeutic capabilities. Hospitals offer access to advanced medications, surgical interventions, and multidisciplinary care, making them the primary point of care for patients with severe intestinal dysmotility disorders. The presence of specialized gastroenterology departments and trained professionals further supports the adoption of therapies in this segment. Clinics and outpatient care centers form the second-largest end-user segment, driven by their increasing focus on early diagnosis and long-term management of intestinal dysmotility disorders. These facilities provide convenient access to medications, monitoring, and follow-up care, allowing patients to manage symptoms without hospitalization. Growing awareness among physicians and patients, coupled with advancements in minimally invasive diagnostic tools, has further boosted therapy adoption in clinics, supporting the overall expansion of the intestinal dysmotility therapy market.

North America is expected to lead the market geographically. The region benefits from advanced healthcare infrastructure, high adoption of innovative therapies, significant investment in research and development, and a growing patient pool with gastrointestinal disorders. For instance, in 2023, Renexxion Ireland Limited (Renexxion), a private biopharmaceutical company, announced that it had filed an Investigational New Drug (IND) application with the U.S. FDA for naronapride to treat gastrointestinal (GI) motility disorders in cystic fibrosis (CF) patients, marking the first step toward clinical trials. Naronapride, a novel pan-GI prokinetic, had shown positive Phase II results in upper and lower GI indications with a safety profile comparable to placebo. This development addressed unmet needs in CF-related GI dysmotility and was expected to boost the growth of the Global Intestinal Dysmotility Therapy Market in this region.

Furthermore, the strong awareness among healthcare providers and patients, coupled with supportive regulatory frameworks, drives the growth of the intestinal dysmotility therapy market in North America. Also, the high prevalence of IBS cases is also fuelling the growth of this market in this region. For instance, Canadian Digestive Health Foundation in June 2025, reported that Irritable Bowel Syndrome (IBS) as a Disorder of Gut-Brain Interaction (DGBI), where dysregulated communication between the gut and brain led to misinterpretation of normal digestive processes as pain. The dysfunction also caused abnormal gut motility, resulting in either slowed or accelerated digestive movement. Disruptions in gut microbiota were commonly observed, worsening symptoms and long-term digestive distress. Canada reported one of the highest IBS prevalence rates globally, at approximately 18%, compared with 11% worldwide, emphasizing the need for awareness, education, and access to science-based resources for affected individuals. Thus, such factors is increasing the demand for Intestinal Dysmotility Therapy treatments, and thus fueling the market’s growth in this region.

| Report Matrics | Details |

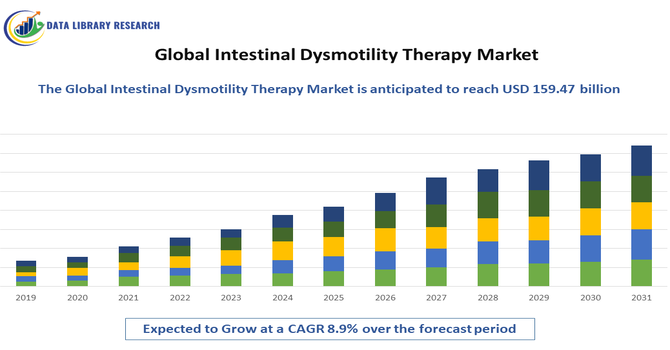

| Market Size Value | USD 159.47 billion |

| Growth Rate | CAGR of 8.9 % |

| Forecast | 2026-2033 |

| Historical data | 2021-2024 |

| Base Year | 2025 |

| Report Coverage | Forecasted revenue, company rating, competitive environment, growth drivers, and trends |

| Segment Coverage | Type, Application, End-User, Geography |

| Regional Scope | North America, Europe, Asia Pacific, Middle East |

| Customized scope | Free customization of reports (With 3 months Analysis Support ) |

| To Learn More About This Report | Request a Free Sample Copy |

The Global Intestinal Dysmotility Therapy Market is characterized by a diverse and competitive landscape, with numerous pharmaceutical and biotechnology companies actively engaged in the development and commercialization of therapies for gastrointestinal motility disorders. These companies range from established multinational corporations to emerging biotech firms, all contributing to the advancement of treatment options for conditions such as gastroparesis, chronic intestinal pseudo-obstruction, and irritable bowel syndrome. The competitive landscape of the Global Intestinal Dysmotility Therapy Market is further shaped by continuous research and development, strategic collaborations, and mergers and acquisitions. Companies are investing heavily in innovative drug delivery systems, novel prokinetic agents, and neuromodulators to enhance efficacy and patient compliance. Additionally, the growing focus on personalized medicine and precision therapies, along with the increasing adoption of advanced diagnostic technologies, is driving differentiation among players, fostering innovation, and intensifying competition, ultimately accelerating the development of more effective and targeted treatments for intestinal dysmotility disorders worldwide.

Key players in the market include:

Recent Development

Q1. What are the main growth driving factors for this market?

The market is primarily driven by the rising global prevalence of chronic gastrointestinal (GI) disorders such as gastroparesis, chronic intestinal pseudo-obstruction, and Irritable Bowel Syndrome (IBS). Significant growth is fueled by technological advancements in diagnostics, including high-resolution manometry, and the development of novel and targeted therapeutic agents, especially biologics and prokinetic drugs. Furthermore, increasing awareness about these conditions and the growing geriatric population, who are more susceptible to GI issues, contribute significantly to market expansion and demand for effective treatments.

Q2. What are the main restraining factors for this market?

The market faces significant restraints primarily due to the complexity and difficulty in diagnosing intestinal dysmotility disorders accurately, often leading to delays or misdiagnosis. Other major factors include the high cost associated with advanced treatments and specialized diagnostic procedures, which limits patient access, particularly in developing economies. Additionally, the limited number of efficacious treatment options for severe or refractory cases and the side effects associated with existing pharmacological agents pose significant challenges to market growth.

Q3. Which segment is expected to witness high growth?

Based on therapeutic approach, the medication segment, particularly the sub-segment for prokinetic agents and biologics/biosimilars, is expected to witness high growth. Prokinetics are vital for improving gut motility, while biologics represent the future for treating underlying inflammatory and autoimmune mechanisms of dysmotility. From a disorder perspective, segments like Chronic Intestinal Pseudo-Obstruction (CIPO) or therapy for specific conditions like diabetic gastroparesis are forecasted to see rapid expansion driven by unmet medical needs and a growing patient pool.

Q4. Who are the top major players for this market?

The global market features key players who often have a strong portfolio across the wider gastrointestinal therapeutic landscape, including Inflammatory Bowel Disease (IBD) and IBS. Top major players include Takeda Pharmaceutical Company Limited, AbbVie Inc., Johnson & Johnson (Janssen Biotech), Pfizer Inc., and Bausch Health Companies (Salix Pharmaceuticals). Other significant companies like Ironwood Pharmaceuticals and AstraZeneca also maintain a strong presence, constantly investing in research and development of new drugs and advanced therapeutic solutions for complex motility disorders.

Q5. Which country is the largest player?

North America, specifically the United States, is consistently identified as the largest player and dominates the global market for intestinal dysmotility therapy. This dominance is attributed to several key factors: a high prevalence of GI disorders, the presence of robust and advanced healthcare infrastructure, high adoption rates of novel and expensive therapies, and favorable reimbursement policies. Furthermore, the region is a major hub for pharmaceutical and biotechnology research and development, which constantly drives therapeutic innovation.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model