Get Complete Analysis Of The Report - Download Updated Free Sample PDF

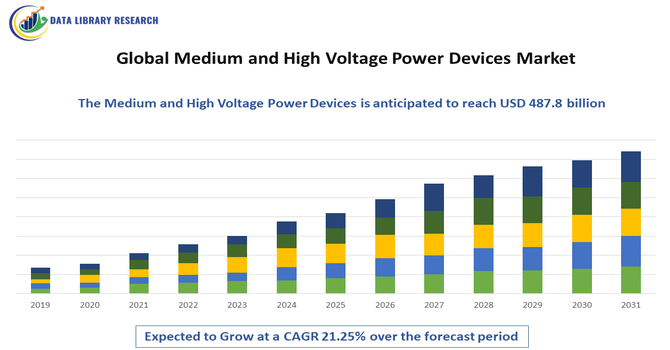

The Global Medium and High Voltage Power Devices Market is experiencing steady growth as industries and utilities continue to modernize power infrastructure and adopt advanced power electronics to meet increasing energy reliability, efficiency, and grid stability requirements. These devices—including IGBTs, MOSFETs, thyristors, insulated gate gate-commutated thyristors (IGCTs), and high-power diodes—are essential for power transmission, smart grids, renewable energy systems, industrial automation, and electric mobility applications. The transition toward renewable energy sources such as solar and wind, along with the rising deployment of HVDC transmission systems, grid automation, and energy storage solutions, is increasing the adoption of medium and high-power switching and control devices.

The Global Medium and High Voltage Power Devices Market is witnessing several emerging trends, with one of the most notable being the rapid adoption of wide-bandgap semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN), which offer higher efficiency, improved thermal performance, and faster switching capabilities compared to traditional silicon-based devices. There is also a growing shift toward integrated and modular power modules designed to reduce system size, improve power density, and simplify deployment in high-voltage applications.

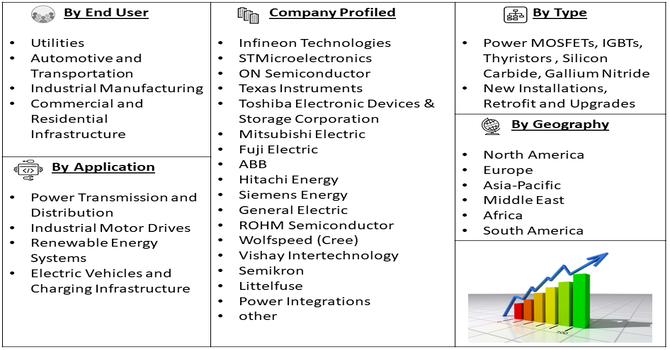

Segmentation: Global Medium and High Voltage Power Devices Market is segmented By Device Type (Power MOSFETs, IGBTs, Thyristors, Silicon Carbide, Gallium Nitride), Installation Type (New Installations, Retrofit and Upgrades), Application (Power Transmission and Distribution, Industrial Motor Drives, Renewable Energy Systems, Electric Vehicles and Charging Infrastructure), End User (Utilities, Automotive and Transportation, Industrial Manufacturing, Commercial and Residential Infrastructure), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report provides the value (in USD million) for the above segments.

For Detailed Market Segmentation - Get a Free Sample PDF

Market Drivers:

The rapid integration of renewable energy sources such as solar and wind, along with increasing investments in smart grid infrastructure, energy storage systems, and high-efficiency transmission networks, is driving strong demand for medium and high voltage power devices to improve power stability, reduce transmission losses, and enable efficient power conversion.

In August 2024, Hitachi Energy called for urgent action to expand global power grids, reduce connection bottlenecks, and accelerate the energy transition through advanced power electronics technology. With 3,000 GW of renewable projects waiting in grid queues and 80 million km of grids requiring upgrades by 2040, the demand for modernized, controlled interconnections grew. This scenario boosted the global medium and high voltage power devices market, driven by rising renewable energy adoption, grid modernization efforts, and the need for stable, efficient, and resilient power systems.

The expansion of electric vehicles (EVs), EV fast-charging networks, and electrified public transport systems, coupled with the growing adoption of automation in industrial processes, is accelerating the need for high-performance power devices like IGBTs, SiC, and GaN modules, which deliver high efficiency, reliability, and thermal stability in high-voltage applications.

In April 2020, ABB announced its role as a supplier of high-voltage-capable chargers for the Volvo LIGHTS project, providing charging systems capable of up to 920 VDC to enable faster charging and improved fleet utilization. The project, a collaboration between Volvo Group, Volvo Trucks, Greenlots, and other stakeholders, demonstrated how battery electric vehicles could optimize freight and warehouse operations, reduce emissions, and enhance air quality. This initiative strengthened the global medium and high voltage power devices market by supporting transportation electrification and industrial automation.

Market Restraints

The sector is challenged by long product qualification cycles, stringent regulatory standards, and complex certification requirements, particularly for applications in power transmission, aerospace, and automotive safety systems. Supply chain instability—especially in semiconductor fabrication, raw material availability, and rare-earth component sourcing—continues to pose risks, leading to extended lead times and pricing volatility. Furthermore, the lack of skilled technical expertise required for integration, maintenance, and system-level calibration creates barriers, particularly in developing economies where infrastructure modernization is still emerging, collectively slowing the full-scale deployment of medium and high voltage power devices.

The global medium and high voltage power devices market has a significant socioeconomic impact by enabling the efficient generation, transmission, and distribution of electricity across industries and communities. These devices support reliable power supply, reduce energy losses, and improve grid stability, which in turn drives industrial productivity, economic growth, and urban development. By creating demand for skilled engineers, technicians, and manufacturing jobs, the market also contributes to employment and technological advancement worldwide.

Segmental Analysis:

Within the device type category, Insulated Gate Bipolar Transistors (IGBTs) hold a prominent share due to their widespread adoption in high-voltage switching applications such as transmission systems, renewable energy inverters, and electric vehicle power modules. Their efficiency, higher power handling capability, and suitability for medium-to-high voltage environments make them a preferred choice over traditional silicon-based devices, especially as demand grows for fast-switching and energy-efficient power conversion technologies.

In the installation type segment, retrofit and upgrade solutions are witnessing growing demand as aging grid infrastructure worldwide requires modernization to support higher load capacity, digital monitoring, and renewable power integration. Utilities and industrial users increasingly prefer retrofitting over full replacement to minimize cost, downtime, and installation complexity, making this segment a key contributor to market expansion.

Among applications, the electric vehicles and charging infrastructure segment is experiencing rapid growth driven by global electrification initiatives, stringent emission reduction mandates, and increasing EV adoption. Medium and high-voltage devices are crucial in onboard chargers, powertrain modules, DC fast-charging systems, and battery management, positioning this segment as a major demand accelerator in the forecast period.

The utilities segment dominates end-user demand as power companies invest heavily in high-voltage devices for grid strengthening, smart meter integration, transformer upgrades, substation automation, and distributed energy management. The transition toward smart grids and renewable-based power generation further amplifies the need for efficient switching, protection, and transmission components, ensuring strong utility-driven growth.

The North America region is expected to witness the highest growth over the forecast period, supported by significant investments in upgrading aging power infrastructure and integrating renewable energy sources into the grid. The region is also experiencing rapid growth in electric vehicle penetration, prompting expansion of charging networks and high-voltage power electronics in transportation.

In November 2025, Amperesand, a global provider in next-generation power infrastructure for AI data centers and critical power applications, closed an USD 80 million Series A funding round co-led by Walden Catalyst Ventures and Temasek. The oversubscribed round included new investors Industry Ventures, Acclimate Ventures, and SG Growth Capital, alongside continued support from Xora Innovation, Material Impact, TDK Ventures, and Foothill Ventures. This funding strengthened the U.S. medium and high voltage power devices market by accelerating the development of advanced, high-efficiency power solutions for AI and critical infrastructure.

Additionally, strong governmental policies promoting energy efficiency, advanced semiconductor innovation, and manufacturing expansion—particularly in the United States—are further accelerating the adoption of medium and high voltage power devices. Thus, together, these factors position North America as a leading contributor to market growth in the coming years.

To Learn More About This Report - Request a Free Sample Copy

The competitive landscape of the Global Medium and High Voltage Power Devices Market is shaped by a mix of large semiconductor manufacturers, specialized power-module producers, and industrial conglomerates competing on device performance (efficiency, voltage rating, thermal management), wide-bandgap technology leadership (SiC/GaN), system-level integration, reliability, and global service/support capabilities.

Key Players:

Recent Development:

Q1. What are the main growth-driving factors for this market?

The market is strongly driven by massive global investment in power infrastructure and the urgent need to integrate more renewable energy sources like wind and solar power into the electric grid. Medium and High Voltage (MHV) devices are essential for efficiently transmitting this electricity over long distances and stabilizing the grid. Furthermore, the push for grid modernization and smart grid technology, which requires advanced components for better power management, significantly accelerates market expansion.

Q2. What are the main restraining factors for this market?

A primary challenge is the high capital expenditure required for purchasing and installing these sophisticated MHV power devices, which can be a barrier for smaller utility companies. The market is also hindered by the complexity and long lead times involved in the rigorous testing and certification processes required for new, high-voltage equipment. Additionally, the fluctuating costs of raw materials, such as copper and specialized alloys, can introduce price volatility and restrain steady market growth.

Q3. Which segment is expected to witness high growth?

The High Voltage Direct Current (HVDC) Transmission segment is expected to see the highest growth. This is because HVDC systems are much more efficient than traditional AC systems for transferring bulk power over great distances, especially from remote renewable energy farms, such as offshore wind. The growing demand for robust grid interconnections between different regions and the increased focus on large-scale solar and wind projects are fueling this significant adoption rate.

Q4. Who are the top major players for this market?

The MHV power devices market is highly competitive and dominated by a few global engineering giants. The top players include ABB, which offers a comprehensive range of power and automation technologies, Siemens Energy, known for its extensive portfolio of high-voltage transmission products, and Mitsubishi Electric. Other key industry contributors are General Electric (GE) and Eaton Corporation, all focusing on developing innovative, smart grid-compatible devices and expanding their global distribution networks.

Q5. Which country is the largest player?

US, in North America is expected to witness the highest growth in the global medium and high voltage power devices market over the forecast period, driven by increasing investments in renewable energy, grid modernization, electrification of transportation, and advanced industrial automation. Strong demand for reliable, efficient, and high-capacity power solutions is fueling market expansion.

Data Library Research are conducted by industry experts who offer insight on industry structure, market segmentations technology assessment and competitive landscape (CL), and penetration, as well as on emerging trends. Their analysis is based on primary interviews (~ 80%) and secondary research (~ 20%) as well as years of professional expertise in their respective industries. Adding to this, by analysing historical trends and current market positions, our analysts predict where the market will be headed for the next five years. Furthermore, the varying trends of segment & categories geographically presented are also studied and the estimated based on the primary & secondary research.

In this particular report from the supply side Data Library Research has conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and SOFT) of the companies that active & prominent as well as the midsized organization

FIGURE 1: DLR RESEARH PROCESS

Extensive primary research was conducted to gain a deeper insight of the market and industry performance. The analysis is based on both primary and secondary research as well as years of professional expertise in the respective industries.

In addition to analysing current and historical trends, our analysts predict where the market is headed over the next five years.

It varies by segment for these categories geographically presented in the list of market tables. Speaking about this particular report we have conducted primary surveys (interviews) with the key level executives (VP, CEO’s, Marketing Director, Business Development Manager and many more) of the major players active in the market.

Secondary ResearchSecondary research was mainly used to collect and identify information useful for the extensive, technical, market-oriented, and Friend’s study of the Global Extra Neutral Alcohol. It was also used to obtain key information about major players, market classification and segmentation according to the industry trends, geographical markets, and developments related to the market and technology perspectives. For this study, analysts have gathered information from various credible sources, such as annual reports, sec filings, journals, white papers, SOFT presentations, and company web sites.

Market Size EstimationBoth, top-down and bottom-up approaches were used to estimate and validate the size of the Global market and to estimate the size of various other dependent submarkets in the overall Extra Neutral Alcohol. The key players in the market were identified through secondary research and their market contributions in the respective geographies were determined through primary and secondary research.

Forecast Model